Ready to run background checks the modern way?

Bankruptcy background checks provide valuable information about a candidate’s financial history. Typically reserved for individuals applying for financially sensitive positions, these checks can help protect your company’s assets and reputation. Whether a bankruptcy filing shows up in a candidate's history or not, all employers need to prioritize compliance with applicable laws and guidelines when using background checks to make employment decisions.

In this guide, we’ll explore what you should know about bankruptcy, when filings may show up on a pre-employment background screening, and the laws governing bankruptcy background checks.

What is a bankruptcy check?

A bankruptcy background check is a search of public records or a candidate's credit reports to determine whether they have filed for bankruptcy. Bankruptcy checks are not usually necessary for every candidate an employer hires. They are most often used by employers hiring for positions in the financial services industry or for positions with access to company assets or sensitive financial information.

Bankruptcy is a legal procedure individuals and businesses may use to discharge, repay, or restructure debt to improve their financial situation. A bankruptcy filing typically begins when an individual or business files a petition in federal bankruptcy court. People often file for bankruptcy because they cannot afford to pay their debts. Depending on the type of filing, the petitioner’s debt may be eliminated or a repayment plan may be developed.

Employers conduct bankruptcy background checks to get an objective picture of a candidate’s financial history, including how they’ve managed credit in the past.

Get a background check today

Common types of bankruptcy

The most common types of business bankruptcies are Chapters 7 and 11, and the most common types of personal bankruptcies are Chapters 7 and 13. Let’s take a closer look at each type that may appear on a bankruptcy background check and when they’re most often filed.

Businesses that file for bankruptcy usually do so under Chapter 7 or Chapter 11 of federal bankruptcy laws. A Chapter 7 filing typically occurs when a company is going out of business. Most of the company’s assets are liquidated, and the proceeds are used to pay its creditors. Non-secured debts that remain after the liquidation are discharged as allowed by law.

Generally, companies that want to stay in business file Chapter 11 bankruptcy. It lets the business owner retain control of and run the business during the bankruptcy proceedings. In a Chapter 11 filing, the company reorganizes its debt to allow the business to repay its creditors over a longer period or reduce the total amount it owes.

There are two types of personal bankruptcy filings—Chapter 7 and Chapter 13. If an individual is eligible to file Chapter 7 bankruptcy, their non-exempt assets are sold to repay their creditors. Certain types of property are exempt from liquidation and won’t be sold—laws vary by state. Unsecured debt that remains after the sale is discharged and doesn’t have to be repaid. However, some debts, such as alimony, child support, student loans, certain taxes, and more, cannot be discharged in a Chapter 7 bankruptcy filing, and the debtor remains responsible for payment of them.

During a Chapter 13 bankruptcy filing, a person's assets aren't liquidated. This type of filing stops foreclosures and repossessions and allows debtors to develop a plan for paying off their debt in three to five years. Any remaining unsecured debt gets discharged at the end of the repayment period. To file for Chapter 13 bankruptcy, a person's combined secured and unsecured debts can't exceed $2.75 million.

Chapter 7 filings are more common than Chapter 13 filings. However, Chapter 13 filings increased by more than 30% in 2022.

Do bankruptcies show up on background checks?

Bankruptcy employment background checks may be included in a comprehensive pre-employment screening, depending on the searches you include for the positions for which you’re hiring. Let’s look at a few of the most common types of background checks and whether bankruptcy filings appear on those reports.

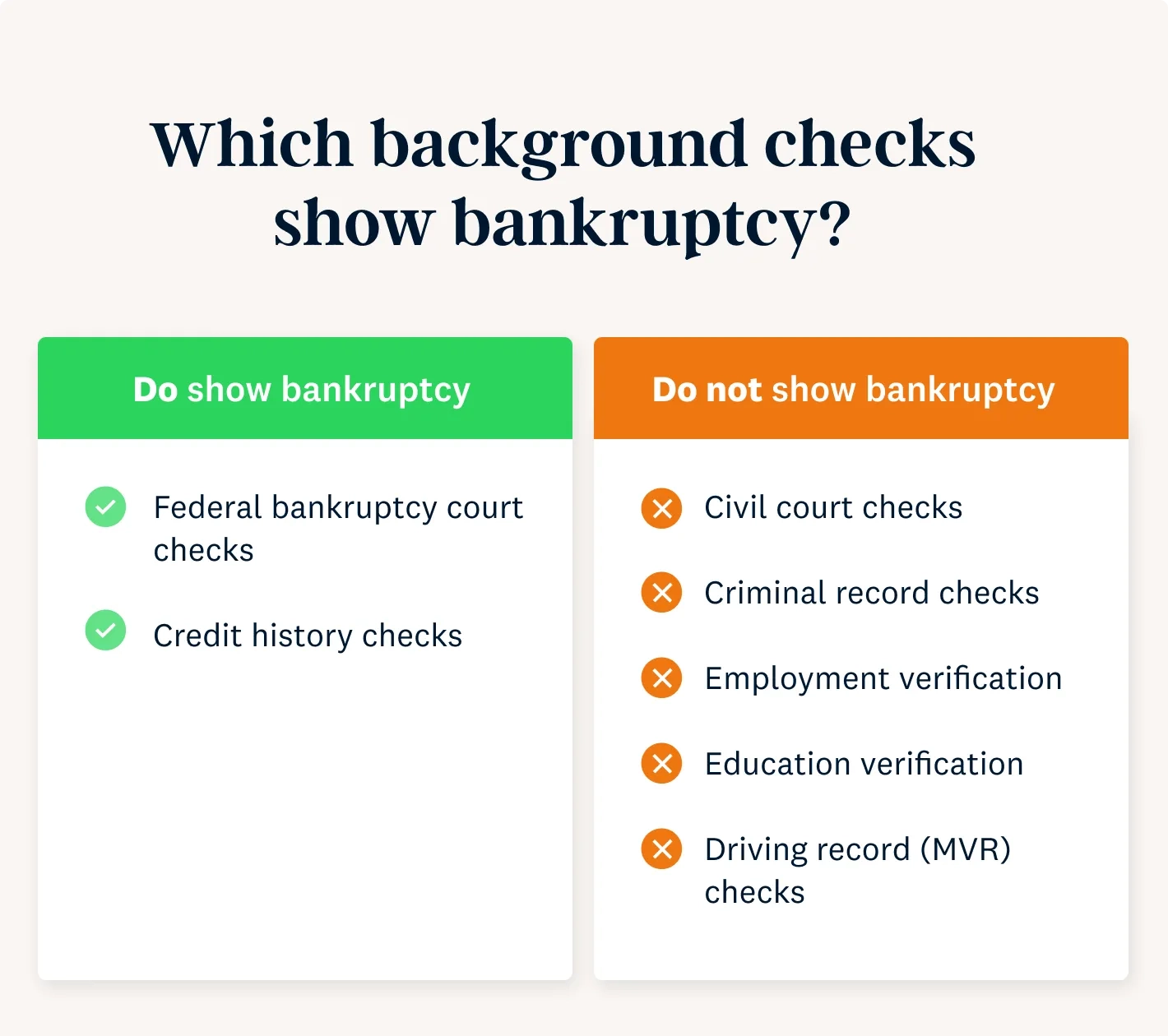

Federal bankruptcy checks search federal bankruptcy courts. Filings for Chapter 7, Chapter 11, and Chapter 13 bankruptcies may appear on this type of check.

Credit checks review a person's credit reports, including payment history, repossessions, foreclosures, and bankruptcies. A credit background check for employment does not include their credit score. Bankruptcies may show up on a person's credit report for up to seven or ten years after the filing, depending on certain factors.

Civil court background checks may search lower and upper civil county courts and federal civil courts. Searches provide information about a candidate's non-criminal legal history, such as claims, suits, and judgments in which a candidate was involved. Their results do not include bankruptcy filings.

Criminal background checks review a candidate’s criminal history and may show arrests, pending criminal cases, and misdemeanor and felony convictions. Bankruptcies will not show up in criminal history background checks.

Employment verification confirms a candidate's employment history, including previous jobs and employment dates with former employers. A bankruptcy filing will not appear during the employment verification process.

Education verification reviews a candidate's academic background, including colleges and universities they attended, enrollment dates, and degrees earned. It does not include bankruptcy filings.

Driving record (MVR) checks examine a candidate's driving history, license status, and safety record. Bankruptcy filings don't appear on MVR checks.

Bankruptcy background check laws

Both federal and state laws regulate how employers may use a pre-employment background check for bankruptcy in employment decisions. Federal law prohibits public employers from considering bankruptcy during the employment process. However, private employers may consider whether a candidate has filed for bankruptcy when making an employment decision—if the bankruptcy is relevant to their job duties and it is allowed by state and local law.

When employers work with a consumer reporting agency (CRA), like Checkr, to conduct a background check, the federal Fair Credit Reporting Act (FCRA) limits the lookback period for credit and bankruptcy checks. Employers may review seven years of a candidate's credit history for positions with a salary of $75,000 per year or less and ten years for positions with an annual salary over $75,000. Bankruptcies may be reported for up to ten years.

Under the FCRA, employers partnering with a CRA must provide candidates with written notice of their intent to conduct a pre-employment background check and receive written consent from the candidate before completing it. Candidates have a right to dispute findings from a pre-employment screening. Employers should follow the adverse action process if they decide not to hire an individual because of information that shows up during a background check.

States may also have laws restricting employers’ use of bankruptcies in employment decisions. For example, California, Oregon, and Maryland prohibit employers from using credit reports to make a hiring decision, except in limited situations.

FAQs about bankruptcy checks

Before conducting a bankruptcy employment background check, it's important to understand how they work, and how you may use them to make hiring decisions. Here are some answers to frequently asked questions.

Bankruptcy background checks can help employers identify qualified candidates, make informed hiring decisions, and protect company assets. Conducting a bankruptcy check on job candidates may help employers feel more comfortable that the individuals they hire will make responsible financial decisions on the job.

A bankruptcy background check typically goes back seven to ten years, depending on the type of bankruptcy filing. No bankruptcies remain on a credit report for more than ten years.

The length of time a bankruptcy stays on a background check depends on the type of filing. Chapter 7 filings remain on credit reports for up to ten years, and Chapter 11 filings stay reportable for seven years.

It depends on the position for which a candidate is applying. Under federal law, it’s illegal for public employers to refuse to hire a candidate because they previously filed for bankruptcy. However, private employers may consider whether a candidate has filed for bankruptcy if state and local laws permit it and if the bankruptcy is relevant to their job duties.

Keep in mind that the FCRA requires employers to follow the adverse action process if they choose not to hire a candidate based on information found in a background check (including a history of bankruptcy).

Get started with an employment background check from Checkr

Bankruptcy background checks can be an important part of comprehensive pre-employment background screenings, especially for employers who work in financial services or hire for positions that involve finance management.

Working with a modern background check provider, like Checkr, can help streamline your background check process, reduce turnaround times, and improve report accuracy. Checkr's easy-to-use platform and built-in compliance workflows help you manage risk and speed up your hiring flow by reducing manual tasks for your team. We offer a wide range background check options—including employment credit checks—and customizable screening packages for businesses of any size. Get started with Checkr.

Get a background check today

Disclaimer

The resources provided here are for educational purposes only and do not constitute legal advice. We advise you to consult your own counsel if you have legal questions related to your specific practices and compliance with applicable laws.

About the author

Jennifer writes about a variety of topics, including background checks, employee benefits, small business insurance, risk management, workplace culture, and more. Her work includes educational articles, blogs, e-books, white papers, and case studies.